Part of the Hawksmoor Group

Part of the Hawksmoor Group

March opened with worrying resonances of the 2008 Global Financial Crisis when two US regional banks collapsed, very quickly indeed, partly due to the efficiency of their new online banking capabilities which allowed a run on the banks to get underway with alarming speed. This was followed up by the troubles at Credit Suisse, Switzerland’s second largest bank, leading to its forced merger with UBS, the largest bank in that country. These cases sent shockwaves through the banking sector worldwide and will lead to additional regulation which in turn may constrain lending and thus slow global growth.

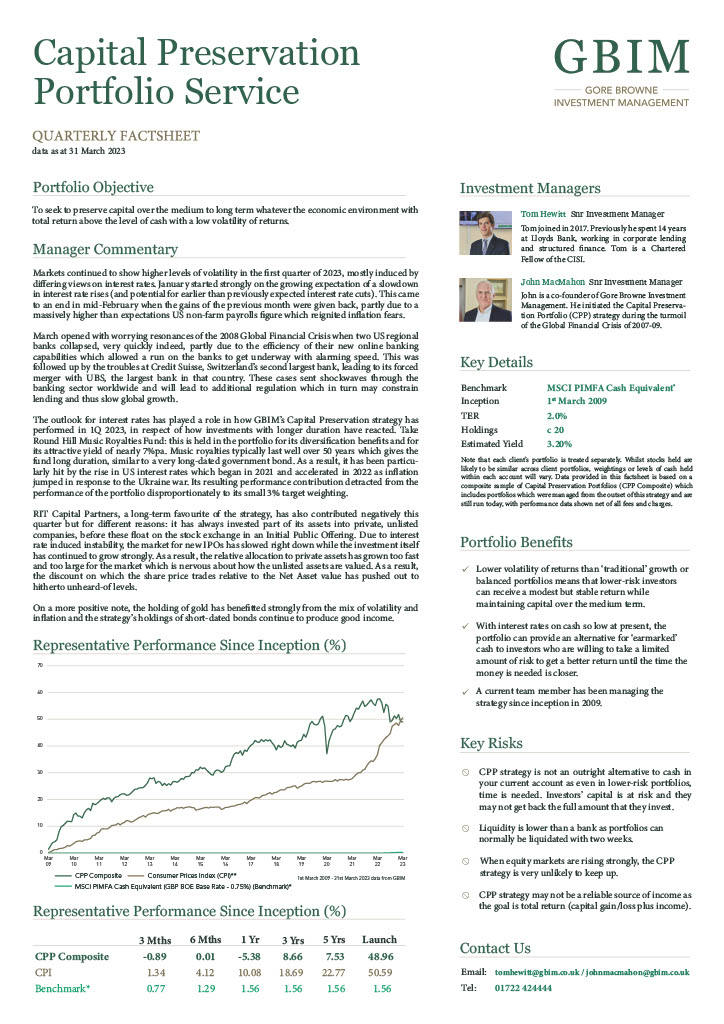

The outlook for interest rates has played a role in how GBIM’s Capital Preservation strategy has performed in 1Q 2023, in respect of how investments with longer duration have reacted. Take Round Hill Music Royalties Fund: this is held in the portfolio for its diversification benefits and for its attractive yield of nearly 7%pa. Music royalties typically last well over 50 years which gives the fund long duration, similar to a very long-dated government bond. As a result, it has been particularly hit by the rise in US interest rates which began in 2021 and accelerated in 2022 as inflation jumped in response to the Ukraine war. Its resulting performance contribution detracted from the performance of the portfolio disproportionately to its small 3% target weighting.

RIT Capital Partners, a long-term favourite of the strategy, has also contributed negatively this quarter but for different reasons: it has always invested part of its assets into private, unlisted companies, before these float on the stock exchange in an Initial Public Offering. Due to interest rate induced instability, the market for new IPOs has slowed right down while the investment itself has continued to grow strongly. As a result, the relative allocation to private assets has grown too fast and too large for the market which is nervous about how the unlisted assets are valued. As a result, the discount on which the share price trades relative to the Net Asset value has pushed out to hitherto unheard-of levels.

On a more positive note, the holding of gold has benefitted strongly from the mix of volatility and inflation and the strategy’s holdings of short-dated bonds continue to produce good income.