Part of the Hawksmoor Group

Part of the Hawksmoor Group

Economies turned out to be far more resilient in 2023 than initially feared: the promised UK recession failed to show, inflation is coming down and rate cuts are forecast for March 2024. Growth in general though remains anaemic, geopolitics is a minefield, and a lot of households are rolling on to eyewatering mortgage bills. We therefore continue to prefer defensive business models, structural growth markets, and prudent debt levels. Helpfully, supply chains are generally functioning again—albeit currently impacted by tensions in the Red Sea. We are now in a destocking cycle as companies no longer feel they need to hoard inventory. For many that will boost cash flow, while for manufacturers like Advanced Medical Solutions (AMS) it’s a short-term hit to revenues. However, AMS has recently signed new agreements with all three of their US distributors for their popular surgical product, Liquiband (used in hospitals for closing/sealing wounds), which will allow AMS to tap into a $270m addressable market that is growing very quickly.

In terms of changes to the portfolios, we exited our position in Learning Technologies (e-learning services to corporate clients) given the threat that Artificial Intelligence poses to their business model. We also took profits from one of our best performers, Ashtead Technology (provider of rental solutions for the offshore energy sector). We reinvested this cash, along with the Instem takeover proceeds, into Tracsis (data solutions to the rail sector), Bango (alternative payment solutions), and Cohort. Cohort is a defence and security engineering company that provides hardware, software, networks, training, and research to the defence industry, with a particular focus on communication systems, surveillance, and electronic/digital warfare. As is the nature of this market, a large portion of revenues come from the UK MOD with the remainder coming from export defence customers and other firms. Cohort’s markets have naturally high barriers to entry (security clearances, regulation, specialist technology) and provide useful diversification to more economically cyclical companies elsewhere in portfolios.

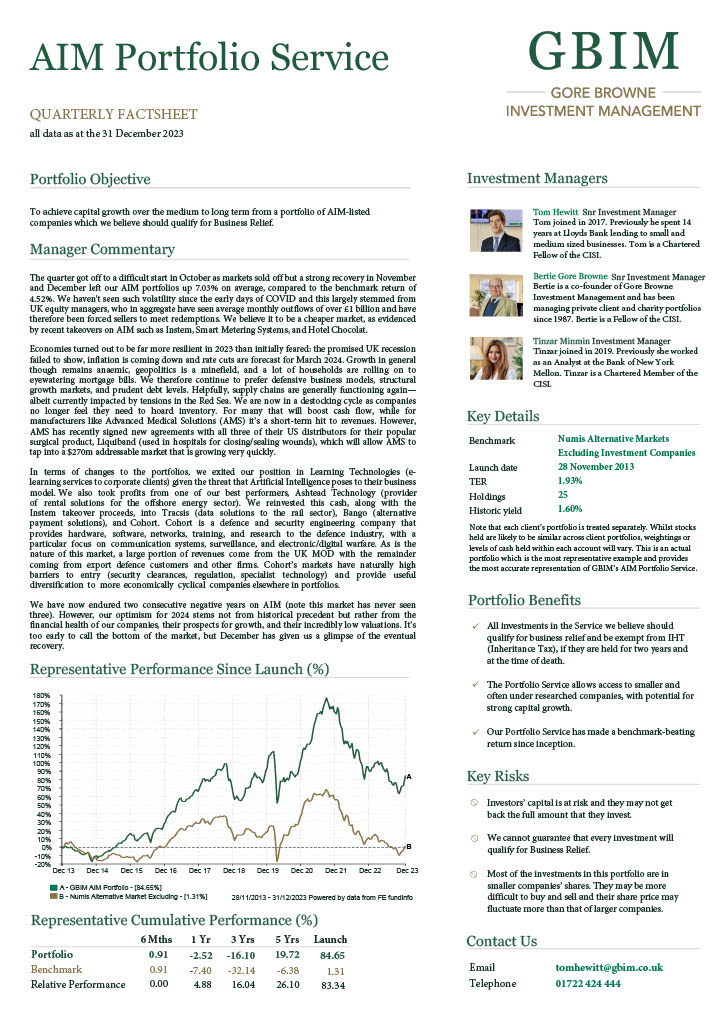

We have now endured two consecutive negative years on AIM (note this market has never seen three). However, our optimism for 2024 stems not from historical precedent but rather from the financial health of our companies, their prospects for growth, and their incredibly low valuations. It’s too early to call the bottom of the market, but December has given us a glimpse of the eventual recovery.